If you’ve ever applied for a car loan, a new apartment, or a credit card, you know that three little numbers hold a lot of power: your Credit Score. But for many, the world of credit reporting feels like a black box. How is it calculated? Does checking it hurt your score? And most importantly, how can you see it without paying a dime?

In this guide, we’ll clear up the confusion around using a Credit Score Checker and show you how to keep your financial reputation in top shape.

Why Should You Check Your Credit Score Regularly?

Your credit score isn’t just a number; it’s a reflection of your financial reliability. Monitoring it regularly is essential for several reasons:

-

Identity Theft Protection: A sudden drop in your score could be the first sign that someone has opened a fraudulent account in your name.

-

Error Detection: Credit bureaus aren’t perfect. Errors on your report can unfairly lower your score.

-

Loan Readiness: If you’re planning to buy a home in 2026, you need to know your score months in advance to ensure you qualify for the best interest rates.

Will Checking My Own Credit Lower My Score?

This is the most common question people ask, and the answer is a resounding NO. When you use a credit score checker to view your own information, it is considered a “Soft Inquiry.” Unlike a “Hard Inquiry” (which happens when a lender checks your credit for a loan application), soft inquiries do not affect your credit points at all. You can check your score every single day if you want to!

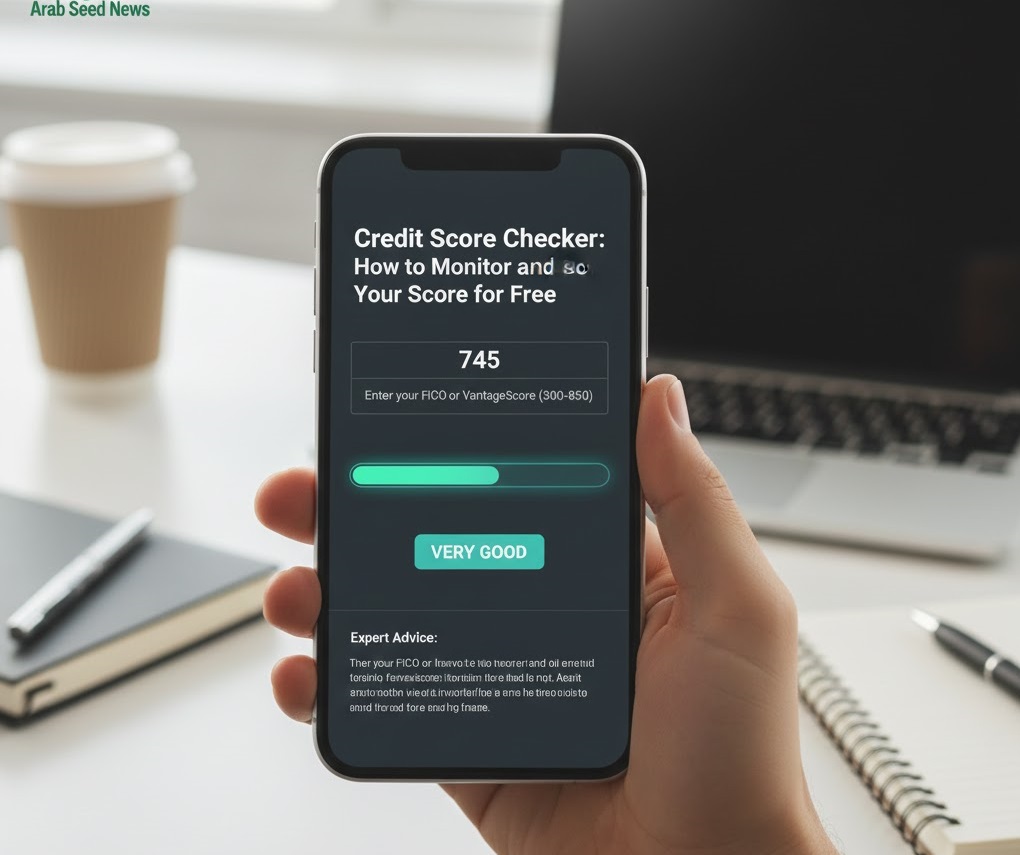

What Do the Numbers Mean? (The 2026 Breakdown)

Most credit score checkers use the FICO or VantageScore models. Here is a general look at where you stand:

-

800 – 850 (Exceptional): You’ll get the lowest interest rates and best perks.

-

740 – 799 (Very Good): You are a highly attractive borrower for most lenders.

-

670 – 739 (Good): This is the U.S. average. You’ll qualify for most loans, but rates may vary.

-

580 – 669 (Fair): You may face higher interest rates or need a co-signer.

-

Below 580 (Poor): You may need to focus on “credit repair” strategies to build your score back up.

How to Improve Your Score Quickly

If your credit score checker shows a number lower than you’d like, don’t panic. Here are the fastest ways to move the needle:

-

Pay on Time: Payment history is the biggest factor (35% of your score). Even one late payment can stay on your report for seven years.

-

Lower Your Utilization: Try to keep your credit card balances below 30% of your total limit.

-

Don’t Close Old Accounts: The length of your credit history matters. Keeping that old college credit card open helps your average “age of credit.”

Frequently Asked Questions (FAQs)

Can I get a truly free credit report?

Yes! Under federal law, you are entitled to a free copy of your credit report from each of the three major bureaus (Equifax, Experian, and TransUnion) via AnnualCreditReport.com.

How often is my credit score updated?

Most lenders report to the bureaus once a month. Therefore, your score typically refreshes every 30 to 45 days.

Does a high income mean a high credit score?

Not necessarily. Your credit score measures your debt management, not your wealth. Someone earning $40,000 a year can have a higher score than someone earning $400,000 if they pay their bills more consistently.

Summary: Take Control of Your Future

Knowledge is power. By using a Credit Score Checker and staying informed, you’re not just looking at a number—you’re building the foundation for your future home, car, and financial freedom. Bookmark our tool and stay on top of your credit health!

Credit Score Analyzer

Enter your FICO or VantageScore (300-850)

580

670

740

850

Related posts:

Fact-Checking Trump’s Prime-Time Address: Reality vs. Rhetoric on the Economy, Immigration, and the ‘Warrior Dividend’

Fact-Checking Trump’s Prime-Time Address: Reality vs. Rhetoric on the Economy, Immigration, and the ‘Warrior Dividend’

Happy New Year 2026: The Ultimate Guide to Wishes, Messages, and Creative Greetings for a Fresh Start

Happy New Year 2026: The Ultimate Guide to Wishes, Messages, and Creative Greetings for a Fresh Start

Breaking Down Trump’s 2025 Economic and Policy Claims

Breaking Down Trump’s 2025 Economic and Policy Claims

Tip Calculator: How Much Should You Actually Tip?

Tip Calculator: How Much Should You Actually Tip?